The Molten Survival Guide. Cannes / Marché du Film 2026.

A field guide to the 2026 market. Enter your name and email to unlock the full read.

Molten Cloud · Cannes 2026

The Molten Survival Guide. Marché du Film 2026.

Hybrid windows, FAST and AVOD, performance-based licensing, AI in rights, the panels you shouldn't miss, and where to drink between meetings. A field guide for the May 12 to 20 market.

11 chapters · ~35 min readMay 12 to 20 · Palais des FestivalsBy the Molten Cloud Marketing Team

Chapter 1

What's New at MDF 2026

The Marché du Film returns to Cannes May 12 to 20, 2026, and this is not a ceremonial year. The programmers have added three new initiatives, repositioned a fourth, and pulled an entire region into spotlight programming. Each change is a signal about where the deal floor is moving.

Eight days, four to six concurrent venues, ~38 official events. The market that fits in a notebook is not the market you signed up for.

The Creator Economy Summit

The single biggest format change at MDF 2026 is the inaugural Creator Economy Summit on Sunday May 17, 10:00 to 13:00, at Plage des Palmes (Goeland Beach). Partnered with ABEL Studios. The summit is half a day, badge-only, and explicitly framed around the intersection of cinema and the creator economy: adapting digital IP into film, scouting talent from platforms, audience engagement strategies that don't fit the traditional acquisition model.

This is the first time Cannes has carved out programming for creator IP entering theatrical pipelines. The structural implication: creator-driven content is no longer competing with studio titles only on streaming platforms; it's competing for the same shelf space, the same buyer attention, and the same rights workflows. If you've been treating creator content as a separate market segment, MDF 2026 is the moment that changes.

Spotlight Screenings, new for 2026

Spotlight Screenings is a new initiative launching in the second week of the market, in the Palais and Riviera screening rooms. The format is built around increased visibility for national line-ups and direct connections to industry buyers, with reduced screening fees and the option to maintain premiere status through confidentiality. If you're acquiring, the morning Spotlight slots are worth tracking; they intentionally sit alongside the buyer-meeting hours rather than competing with them.

Japan, Country of Honour 2026

Japan takes the Country of Honour position for the full duration of the market (May 12 to 20). Partners are METI, JETRO, and UniJapan. The programming is cross-cutting: a co-hosted Opening Night, dedicated panels and showcases throughout the week, with a particular emphasis on Japanese animation and genre cinema, and a Japan Country of Honour breakfast at the Producers Club on May 17 (09:00 to 10:30, Producers Network badge required).

The implication for distributors and rights holders: Japanese IP gets concentrated buyer attention this year, both for acquisition and for co-production conversations. APAC deal flow signals from Cannes are usually 6 to 12 months ahead of where the broader market is reading them.

The Immersive Market

The Immersive Market is a new initiative running out of the Carlton Hotel in a 450 square-metre venue accommodating up to 225 participants per session. Pitching sessions, workshops, panels, and the Immersive Competition (the first of its kind at a major international festival, designed for shared audience experiences). The programming sits under Cannes Next.

This matters for rights conversations even if you don't sell VR or location-based experience titles. Immersive content creates entirely new revenue lines (venue royalties, per-experience licensing, interactive engagement metrics) and the rights structures the industry settles on at MDF 2026 will become the templates the rest of distribution copies in 2027.

AI for Talent Summit

The AI for Talent Summit lands May 15 to 16, also at Plage des Palmes, under the Cannes Next umbrella. Two morning sessions (10:00 to 13:00 each day), invitation only, with access reserved for qualified C-level executives, investors, senior tech professionals, and select media. Topic mix: AI in production workflows, ethical and responsible AI use, real-world use case showcases.

If you've been telling yourself that the AI conversation at film markets is still a topic conversation rather than a contract conversation, the Summit's existence is the evidence that this is no longer true.

What this all adds up to

Four new or repositioned programs in one market, all addressing the same underlying shift: the buyer side and the rights side of the industry are restructuring at the same time, and the structures that worked in 2024 (single all-rights deals, simple FAST/AVOD passes, AI as a future topic, creator content as a separate channel) don't hold in 2026.

The rest of this guide is about the operational reality those new programs reveal.

Sidebar. France is involved in 81% of Competition films at the 79th Festival de Cannes (17 of 21), up from 64% in 2025 and 55% in 2024. The financing pattern that powers Cannes is also the financing pattern that powers most of what's bought at the Marché. Worth keeping in mind during meetings.

Chapter 2

Consolidation and the New Buyer Map

The buyer side of the international market has compressed faster in the last 18 months than at any point in the past decade. Walk into the Palais this year and you are negotiating with a different set of names than you were at MDF 2024. The map has redrawn itself, and most slate decks have not caught up.

What just happened

The headline event in 2025 and 2026 was the Netflix and Warner Bros. Discovery transaction, valued at $82.7B, collapsing through, followed almost immediately by Paramount's $110.9B counter-offer. Whatever combination of those entities ends up walking the Croisette in 2026 will set the buyer-concentration baseline for the next decade.

The less-discussed event was the Rightsline rollup. FilmTrack was acquired in June 2024. RSG Media followed in September 2024. The enterprise rights and royalties tier, which used to host three major vendors competing for studio business, is now effectively one company. If you sold to one of them in 2023, you are integrating with a different posture in 2026.

These two consolidations are unrelated, but they describe the same market: at the top of the stack, fewer counterparties, larger deals, longer integration cycles, and more leverage concentrated in fewer hands.

The new buyer map at MDF 2026

Walking the Marché this year, your meeting list looks something like this.

Major streamers. Netflix, Amazon, Apple, Disney, and the post-deal Warner Bros. Discovery/Paramount entity (whatever shape it lands in). Output deals are increasingly structured around hybrid windows rather than blanket SVOD passes.

FAST and AVOD aggregators. Pluto, Tubi, Roku Channel, Samsung TV Plus, LG Channels, Sling Freestream, Local Now. Plus territory-specific FAST platforms multiplying across Europe, LATAM, and APAC. Most distributors at MDF 2026 will leave with more new FAST/AVOD conversations than SVOD ones.

Regional aggregators. Filmin (Spain, LATAM), Mubi (global, curated), Curzon (UK), and a long tail of national platforms with sharp curation and short-term licensing patterns.

Library acquirers. This is the category that did not really exist at MDF 2023. Allegro Finance announced a $500M senior credit facility for film and TV production with Elliott Advisors in March 2026. MediaHedge (parent of FilmHedge) launched an up-to-$200M JV credit fund with a New York asset manager in April 2026. Hipgnosis-style funds are now buying backend participation rights and residual streams as financial assets. They are at Cannes 2026, and they read rights data the way bond analysts read covenants.

What this means in the room

The first-order effect of consolidation is obvious: fewer buyers. The second-order effect is the one that catches mid-size distributors out: when the buyer side compresses, every remaining deal carries more rights complexity, not less. Output deals turn into multi-window deals. Single-territory SVOD passes turn into pan-regional deals with carve-outs. Holdback layers stack. FAST follows SVOD which follows PVOD which follows theatrical, and the timeline is different in every territory.

What is not happening: mid-size distributors are not dying. The companies clearing the bar at MDF 2026 are the ones that have invested in operational precision. They walk into meetings able to say what's available in any territory, in any window, after any holdback expires, in real time. They send post-meeting deal memos within 24 hours, not 5 days. They reconcile rev shares from 12 platforms in a single dashboard. The deal flow follows the precision.

The companies that are struggling are not the ones with smaller catalogs. They are the ones still answering rights questions with "let me check and get back to you." In 2026, that sentence is the meeting ending.

Sidebar. Cristian Mungiu's Fjord in this year's Cannes Competition is a 6-country co-production: Romania, Norway, Denmark, Finland, France, Sweden. Even arthouse is now a multi-territory rights problem. The middle of the market has moved further in the same direction.

What to watch for at MDF 2026

Three signals that will tell you where the buyer map is going next.

First, how Investors Circle (Saturday May 16, Sunday May 17, Plage des Palmes) talks about library valuation. If institutional buyers are pricing rights catalogs against structured data rather than narrative pitches, you have your answer about where due diligence is heading.

Second, what comes out of the Streamers Forum keynotes. The shift from output deals to title-by-title acquisition (or vice versa) gets signaled there before it shows up in trade press.

Third, who's at the Producers Network breakfasts. The composition of those rooms (May 13 EUFCN, May 14 WIFT Africa, May 15 CCIDA and HKFDC, May 16 Hellenic and TIFF, May 17 Japan, May 18 APROFI) tells you which territory funds are deploying capital in 2026 and which are pulling back.

Chapter 3

Hybrid Windows as the New Standard

The all-rights deal is over. Theatrical opens the window. PVOD lands as early as Day 30 in some territories and as late as Day 90 in others. SVOD enters at staggered points by territory. FAST and AVOD pick up when the higher windows clear. Every line on that timeline is a separate rights obligation, a separate revenue stream, and a separate place where the deal can break.

This is the operational reality of MDF 2026, and it is the chapter most distribution teams underestimate.

The Universal signal

In March 2026, Universal committed to a minimum five-weekend theatrical window in 2026 and a seven-weekend window starting in 2027, formalizing a release strategy it had been running on a per-title basis since the post-pandemic 17-day-window era. The trade press read it as friction, a return to old release rules. That misreads what happened. Universal did not lengthen its theatrical window because exhibitors asked nicely. It did so because it can monetize Day 35 PVOD differently than Day 17 PVOD, and because longer theatrical creates better leverage with streaming partners on the back end.

The lesson for everyone else at MDF 2026: windows are not constraints, they are pricing mechanisms. The studio that controls the window timeline controls the deal.

One title, three timelines

Take a hypothetical title with a global theatrical release on June 5, 2026. Here is what its window timeline looks like across three territories.

Territory

Theatrical

PVOD

SVOD

FAST/AVOD

Germany

Day 0

Day 60

Day 270

Day 540

Brazil

Day 0

Day 30

Day 120

Day 365

Japan

Extended (Day 0 plus reissues through Day 180)

Day 90

Day 365

Day 730

Same title. Three completely different rights timelines. A single PVOD deal that says "available globally Day 60" is a deal that violates Brazil's earlier PVOD launch and Japan's later one. A holdback structure that's clean in Germany is a holdback violation in Brazil. The buyer in any one of these territories is going to ask you, in the meeting, what their window position is. If you are not answering from a system that knows the answer for all three territories at once, you are guessing.

Why this breaks legacy systems

The systems most distributors are running on (Excel grids, the old Rightsline interface, custom Access databases) were designed for a world in which a title had one or two windows per territory and the relationships between windows were stable. Hybrid windowing breaks all three of those assumptions.

Holdbacks compound. A SVOD holdback on PVOD interacts with a FAST holdback on SVOD, which means that the FAST window in any territory is contingent on every higher-tier window's clean expiry. Tracking that across 30 titles and 100 territories is a four-dimensional problem (title, territory, window, time). Spreadsheets are two-dimensional.

Territory windows interact across borders. Pre-sales of European rights come bundled with pan-regional carve-outs. A Spanish theatrical window affects Latin American SVOD timing because the same buyer is often involved in both. If your rights system can't see across territories, you don't catch the conflict until a buyer asks about it.

Window expiries trigger new avails simultaneously. When the FAST window for 80 catalog titles opens on the same day, you don't have time to prepare 80 separate avails grids. You either have a system that auto-generates them or you lose the FAST aggregator's first-look position to a faster competitor.

The new buyer question

Here is the change in language that tells you the most about MDF 2026. The question used to be: "Is this available in Germany?" The answer used to be: "Yes" or "No."

The question now is: "What's the exact rights position for this title in Germany, after Q3 2026, given the current holdbacks and any pending PVOD extensions?" The answer the buyer expects is a structured one, in 30 seconds, with the holdback dates visible.

Distributors who can answer that question in real time, in the room, close deals at MDF 2026. Distributors who cannot, schedule a follow-up call for the following week, by which point the buyer has had the same conversation with three other companies and the urgency has moved on.

What to do about it before MDF 2026

Three concrete actions worth taking before May 12.

First, audit your holdback database for any title in your top 20 by deal value. Confirm that the holdback dates match the underlying contracts and that you have a single source of truth, not three different versions in three different files.

Second, prepare avails snapshots for your priority titles in your priority territories with the windows broken out. Theatrical, PVOD, SVOD, FAST, AVOD. If the snapshot looks unclear to you on May 11, it will look unclear to a buyer on May 13.

Third, designate someone on the team as the holdback authority during the market. Every meeting will have at least one window question. Whoever is in the meeting needs an instant escalation path to a person who can verify the answer before the buyer leaves the room.

Hybrid windows are not a structural anomaly. They are the structure. The companies that internalize this in 2026 are the ones still in business in 2030.

Chapter 4

FAST and AVOD in Every Deal

In 2024, you could walk a film market without engaging seriously with FAST and AVOD. You can't in 2026. Every catalog conversation now ends with a version of "and what about FAST?" and the answer matters more than the question used to.

This chapter is about why that's true and what it changes operationally.

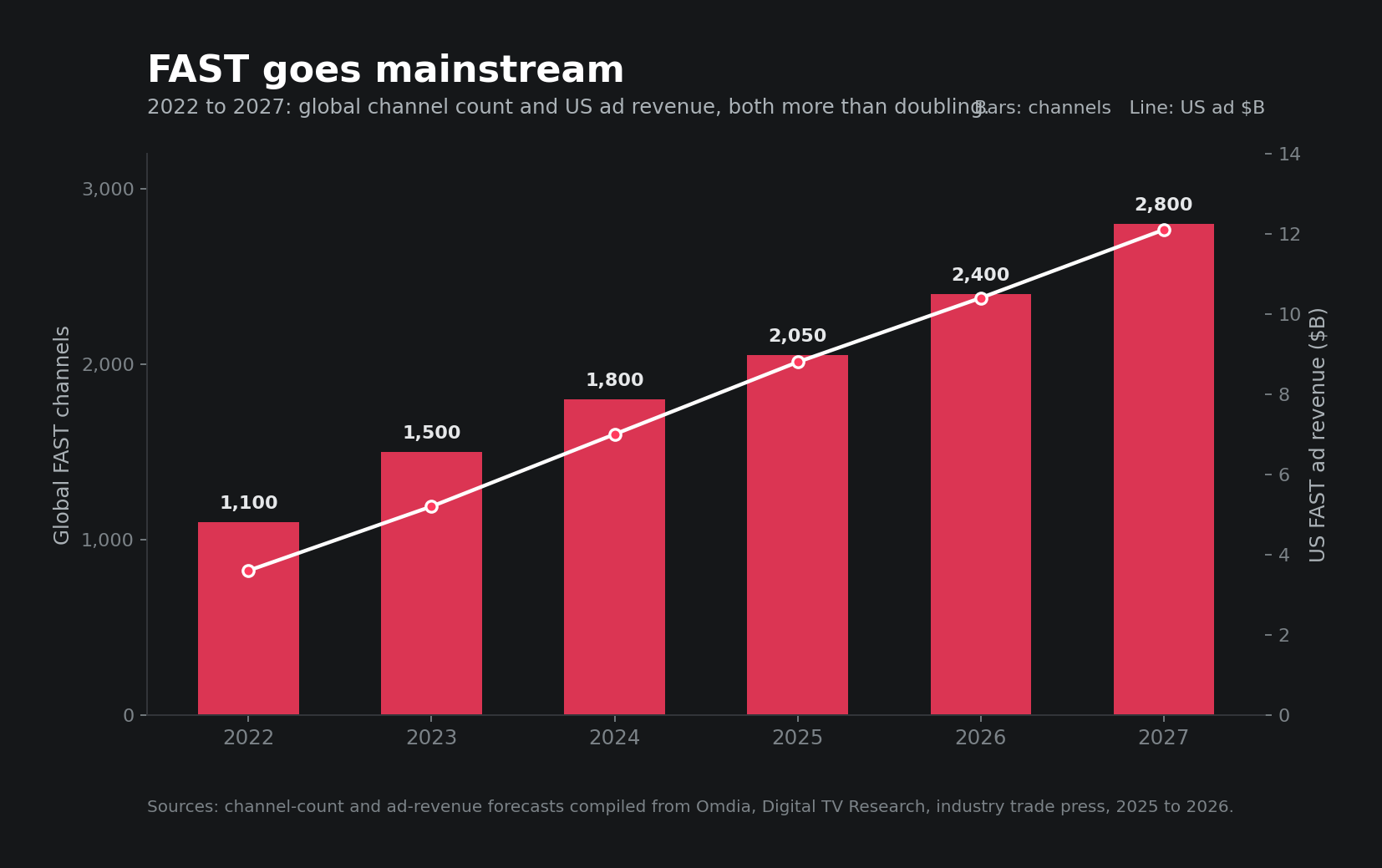

The numbers worth quoting

AVOD revenue for film and TV series is forecast to reach $70B globally by 2027, up from $33B in 2021 (Research and Markets). Global FAST channel revenue is forecast to triple to roughly $12B by 2027 (Omdia). Gracenote tracks approximately 1,850 active FAST channels globally as of Q3 2025, up 76% from 2023 and growing at roughly 14% per year. Revenue shares between distributors and platforms typically sit between 40% and 65%, with most major-platform deals clustering at 50/50 or 55/45 in the platform's favor on prime ad inventory.

These are not future projections; they are forecasts based on growth rates already visible in 2026 reporting. The acquisition budgets behind those numbers are already at MDF.

Global FAST channel count and ad revenue, 2022 to 2027. ~1,850 channels in Q3 2025, on track to clear 2,000 in 2026; revenue tripling to $12B by 2027. Sources: Omdia, Gracenote, Research and Markets.

The license length problem

Traditional SVOD output deals run 7 to 10 years. FAST and AVOD deals run 1 to 3. That difference looks small on paper. It is enormous in practice.

A 7-year SVOD deal goes into your rights system once and stays there. A FAST license goes in, runs for 18 months, expires, and either renews on slightly different terms or moves to a competitor. Across a catalog of 30 titles, a mid-size distributor in 2026 has 50 to 80 active FAST and AVOD licenses at any given time, and 15 to 25 of them are renewing or expiring in any given quarter.

That is not a portfolio. That is a continuous administrative motion. The companies handling it well have automated the renewal calendar. The companies handling it badly are losing two months of revenue per title per cycle to expiry gaps nobody flagged.

The platforms in the room at Cannes 2026

The platforms that matter at MDF this year, ranked roughly by where the conversations are happening:

Pluto TV (Paramount-owned). Largest US FAST audience, expanding aggressively in Europe and Latin America.

Tubi (Fox-owned). Hit profitability in 2024 and is now in the catalog acquisition mode that sets terms for the rest of the AVOD market.

Samsung TV Plus, LG Channels, Roku Channel. The platform-as-distribution category. Pre-installed on TVs, low friction, ad-supported, increasingly programming first-windows rather than only catalog tail.

Sling Freestream, Local Now. US-centric, niche-specific, often the right home for genre or regional library titles.

Territory-specific FAST aggregators. Filmin (Spain, LATAM), Rakuten TV (Europe), AsianCrush (US/APAC), and a long tail of national and regional FAST platforms multiplying across Europe, MENA, and Asia.

Most of these will be at the Marché in some form. The ones that aren't will be on Cinando running outreach in parallel.

Why this breaks legacy royalty pipelines

The accounting reality of FAST and AVOD is that you don't get paid a license fee. You get paid a percentage of advertising revenue, calculated against viewership, reported on the platform's cadence, in the platform's chosen format.

That changes everything downstream. Every platform reports differently. Some are monthly, some quarterly, some real-time. Some report by territory, some only at the regional level. Some define a "view" as 30 seconds of playback, some as 75% completion. Some include reduced-rate inventory in the rev share, some don't. The metric definitions are different across platforms even when the platforms are owned by the same parent company.

For distributors, this means royalty calculation across a portfolio of FAST and AVOD licenses requires a system that can ingest 12 to 20 different reporting formats, normalize them into a single revenue model, and verify the platform-reported numbers against independent benchmarks. Most rights and royalty systems sold before 2022 cannot do this without months of integration work.

Sidebar. Molten Insights data on multi-platform deal trends shows that the average number of distinct platforms per title in distribution has more than doubled between 2022 and 2026. The growth is concentrated almost entirely in FAST and AVOD additions, with traditional SVOD shares roughly flat.

What this looks like in a Cannes meeting

A typical 2026 conversation with a FAST or AVOD aggregator at MDF lasts 20 to 30 minutes and ends one of two ways. Either you have a clean answer to "which titles in your catalog are available for FAST in [territory] starting [date], and what windows are clear after [holdback date]," in which case the meeting moves to terms. Or you don't, and the meeting ends with "send me the avails when you have them," which translates to "we will probably never speak again."

The buyer is not testing your slate. They are testing whether you can transact at the speed FAST and AVOD economics require. License lengths are short, deal velocity is high, and the platforms that close fast win the inventory.

If your distributor team can't answer that question in 30 seconds for your top 50 catalog titles by May 11, the most useful thing you can do this week is build the avails snapshots. They are the difference between a closed deal at MDF 2026 and a Cinando lead that stays open through MIPCOM.

Chapter 5

Performance-Based Licensing

A licensing fee that depends on viewer engagement is not a contract. It is a data pipeline. That is the single sentence that explains why performance-based licensing has gone from a streamer-side experiment to a structural feature of the 2026 market in roughly 24 months.

If your team is at MDF this year and you are still treating performance terms as a special case, this chapter is the one that costs you a deal.

What changed

Through 2023, the dominant licensing model was a fixed upfront fee, sometimes with bonus tiers tied to renewal or breakout performance, but with the substantial economics locked in at signing. The buyer paid; the distributor delivered; the relationship moved on.

Through 2024 and 2025, that model fractured. Streamers and FAST platforms started asking for, and getting, deal structures where the fee depended directly on viewership, completion rates, repeat-viewing metrics, or a per-minute-streamed calculation. The reasons are obvious from the buyer side: ad-supported platforms cannot pay fixed fees against unpredictable revenue, and SVOD platforms got tired of paying premium fees for titles that underperformed their library averages.

The reasons it became real for distributors are less obvious. They are about who has the leverage. When buyers are concentrated (see chapter 2) and ad revenue is volatile, the buyer's negotiating position is stronger, and the deal terms move toward shared risk. Performance-based licensing is risk-sharing. It is not going away.

Three problems, all data problems

Performance-based licensing introduces three distinct operational problems, and most distributors are not solving any of them well in 2026.

The reporting problem. Every platform reports differently. Pluto reports monthly, Tubi quarterly, Samsung TV Plus on a hybrid cadence, smaller platforms whenever someone gets around to it. The metric definitions vary across the same platform's territories. The data formats are inconsistent. Some platforms expose dashboards; some send CSV exports; some send PDFs that have to be parsed by hand.

The first thing a distributor with a portfolio of performance-based deals needs is a normalization layer. Pull data from every platform on its own schedule, transform it into a single internal model, store it against the deal, and trigger the royalty calculation. Spreadsheets cannot do this. A staff member typing numbers into a master file once a quarter is the failure mode the modern royalty system was designed to replace.

The verification problem. When the platform reports the number, who checks it? The honest answer at most distributors in 2026 is: nobody, until something looks wrong, at which point it is months too late. Performance-based deals require independent verification. That means cross-referencing platform reports against external benchmarks (Parrot Analytics, Ampere, Samba TV), against competing-territory reports for the same title, and against your own historical patterns for similar titles.

You don't need to challenge every number. You need to be able to challenge the ones that don't match your model.

The infrastructure problem. Legacy royalty systems were built around fixed fees with bonus thresholds. They were not built to compute royalties from millions of streaming events ingested across 12 platforms, normalized to a single revenue model, applied against rolling rate cards that vary by territory and by ad inventory tier. The systems sold before 2022 are not extending into this. They are blocking it.

A concrete example

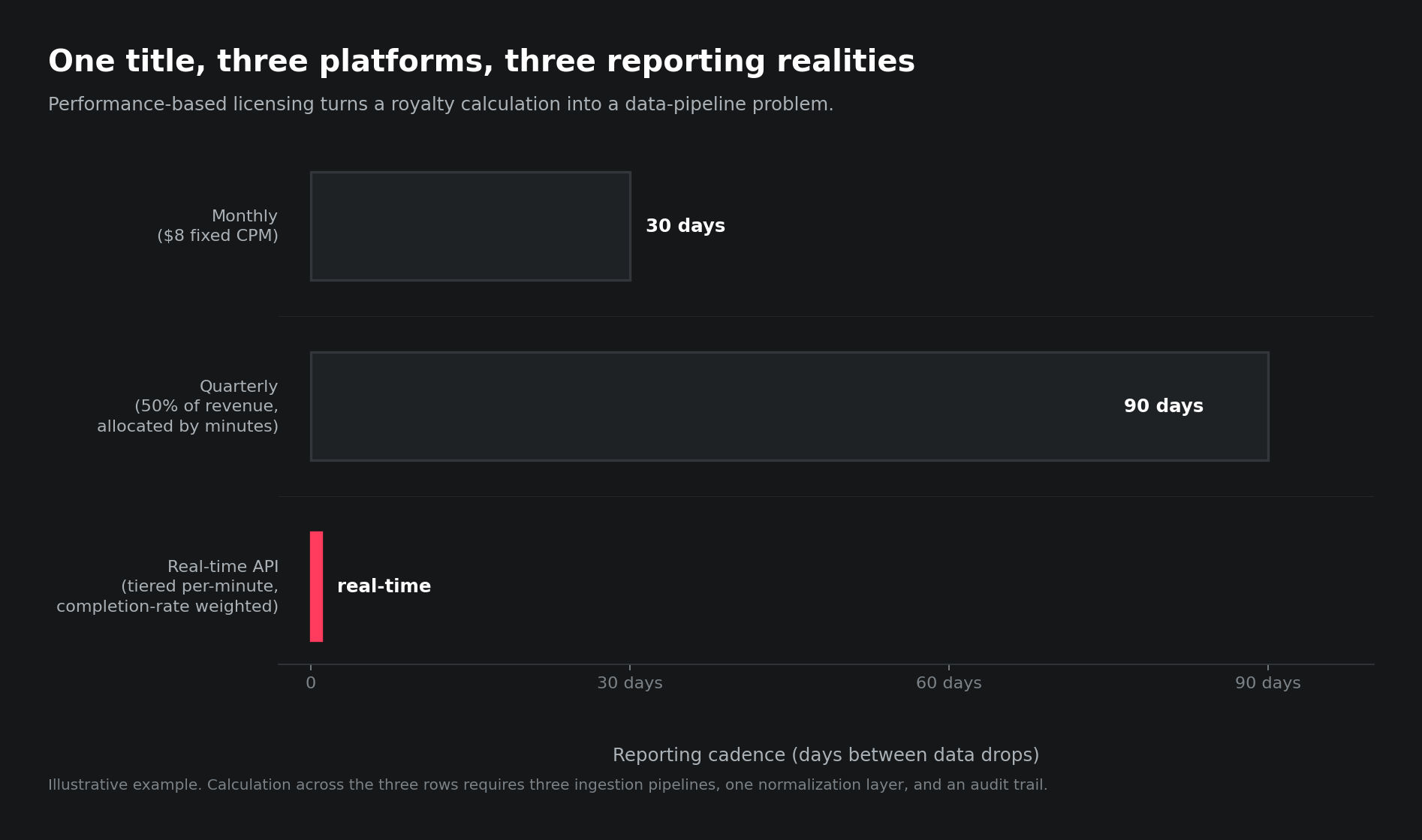

Take a single title, licensed across three FAST platforms, with three different performance structures.

Platform A reports monthly, paying a fixed CPM ($8) on each ad impression delivered against the title.

Platform B reports quarterly, paying a 50% share of total platform ad revenue allocated proportionally by total minutes-streamed, with the title's minutes counted against a rolling 90-day window.

Platform C reports in real time via API, paying a tiered rate per minute streamed: $0.04 per minute for the first 10,000 minutes per month, $0.06 per minute thereafter, with completion-rate multipliers that adjust the per-minute rate up or down by 25%.

To calculate this title's quarterly revenue accurately, you need three different ingestion pipelines, three different revenue formulas, a normalization model that lets you report total title revenue as a single number, and an audit trail that shows exactly how each platform's revenue was derived. None of this is theoretical. This is a normal title in a normal 2026 catalog.

Most distributors are calculating this on a quarterly best-effort basis with at least one number guessed. The ones who aren't are the ones who built infrastructure for it before they needed to.

Three platforms, three reporting cadences. Performance-based licensing turns a royalty calculation into a data-pipeline problem.

What to bring to MDF 2026

If you are walking into a meeting with a streamer or a FAST aggregator and you expect performance terms to come up, three things are worth having ready.

A clear summary of how your team handles platform reporting, in plain language. The buyer is asking. They want to know if the rev share they negotiate will actually be calculated correctly six months later.

A sample royalty statement from a current performance-based deal, anonymized if needed, that demonstrates the level of granularity your reporting can support. This is the equivalent of a financial statement in a fundraise. It is the credibility document.

A position on verification. Are you running independent checks on platform-reported numbers? If yes, with what tools? If no, why not? The buyer will not ask this directly, but it will affect the rate they offer.

Performance-based licensing is here. The companies that bring clean reporting infrastructure to Cannes 2026 close deals. The ones that don't get politely deferred to MIPCOM, then to AFM, and eventually out of the buyer's consideration set entirely.

Chapter 6

AI in Rights Conversations

AI showed up at MDF 2025 as a topic. At MDF 2026 it shows up in your contracts. That single sentence is the most useful framing available for the conversations you'll have on the Croisette this year about AI in rights and royalties.

What changed in 12 months

In May 2025, "AI in distribution" was a panel topic. Speakers debated training data, deepfakes, and whether AI would meaningfully change the deal flow. Most of the room left the panels with the same view they walked in with.

In May 2026, AI is in the deal memos. Entertainment lawyers are now recommending nine or more standard AI clauses in every production contract: training data consent, digital replica rights, output ownership, AI-generated content disclosure, compensation structure for AI-augmented performances, takedown obligations, residual treatment for synthetic performers, indemnity allocation, and territory-specific compliance with emerging legislation. Rodriques Law's 2026 contract template guidance is one of the most-cited references. The IFTA model agreements will catch up, but they're behind.

The artist representation agreement, augmented. Every AI clause becomes a rights record. The contract that fits on paper now also lives in your system.

The implication for distributors is simple. Every title acquired in 2026 carries more rights data than the same title would have carried in 2024. Every contract has more clauses. Every clause has implications that need to be tracked in the rights system, not held in someone's memory.

The Tilly tax and what it means

The most concrete signal of where this is heading is SAG-AFTRA's Tilly tax proposal, raised during the 2026 bargaining cycle. The mechanism: a per-use royalty on synthetic performers, structured similarly to traditional residuals but triggered by every distinct use of an AI-generated likeness.

Whether the Tilly tax lands in its proposed form or in a modified version, two structural facts are now baked in. First, AI-generated performers will require the same rights infrastructure as human ones, with consent logs, usage tracking, and per-use compensation flows. Second, the No Fakes Act and the EU AI Act create territory-specific compliance obligations that have to be tracked at the title-territory level.

Operationally, that means every title with synthetic performance elements (even partial, such as de-aging or voice cloning) carries new metadata: which performer, what consent was logged, what jurisdictions allow what uses, what royalty is owed per use. None of this fits in a comments column on a rights spreadsheet.

Back-catalogs as AI training data

The other AI conversation that lands in 2026 is about back-catalogs as training datasets. The legal question of whether film and television libraries can be licensed for AI training (and at what rate) is unresolved in most jurisdictions, but the licensing conversations are happening now. AI model companies are negotiating, library owners are considering, and the deals being struck in 2026 will set precedents that older contracts did not anticipate.

If your back-catalog rights agreements were signed before 2022, they almost certainly do not address AI training rights. That creates a clean opportunity (the rights are technically not granted to the buyer, so they can be re-licensed) and a clean risk (if the rights chain is unclear, both you and the AI company are exposed).

Distributors and library owners walking into MDF 2026 with structured rights data, including chain-of-title clarity, are the ones in a position to negotiate AI training licenses with confidence. The ones with messy rights records are the ones whose deals stall on legal review.

What to bring to the conversation

If AI is going to come up in your buyer meetings at MDF 2026 (and it will), three things are worth being ready for.

A clear position on AI in your acquired titles. Which titles have AI-augmented elements, what consent records exist, what disclosure obligations apply per territory.

A framework for new acquisitions. What AI clauses you require in production contracts going forward, and how you operationalize them in your rights system.

A point of view on AI training rights for back-catalog. You don't need to have closed deals. You need to have considered the question, and to be able to discuss it without wincing.

The companies that come into Cannes 2026 with AI as a structured rights conversation, not an existential one, are the companies the smarter buyers want to work with.

A note from Molten Cloud

Meet us at the Marché. May 12 to 18.

We're at Cannes through the first week of the Marché. If hybrid deal structures, FAST and AVOD royalties, performance-based licensing, or the consolidation effect on mid-size distributors are live conversations on your side, drop us a message. We'll find a coffee on the Croisette.

The Marché du Film 2026 official programme runs at four to six concurrent venues from May 12 to May 20, with peak density between Friday May 15 and Sunday May 17. There are roughly 38 official events across the major tracks (Summits, Communities, Spotlight Programs, Pitching, Training, AFCI Power of Place sessions). Most attendees will get to maybe 8 of them. The picks below are the ones that pay back the time investment for a distributor, sales agent, producer, or rights professional working in the 2026 market reality this guide describes.

Organized day by day. Each pick has the format: title, day and time, venue, badge requirement, why it matters, and who it's for.

Four to six concurrent venues, ~38 official events, eight days. The math says you'll get to eight of them. Pick well.

MDF 2026 · Programme at a glance

Top picks in red. Ongoing tracks in grey. Peak density runs Fri to Sun.

International Film Finance ForumMain Stage, Riviera

AI for Talent SummitPlage des Palmes

Global Film Commission Network SummitMain Stage, Riviera

Investors CirclePlage des Palmes

Japan IP MarketArt Explora catamaran

Spotlight AsiaPalais Stage / Producers Club

Cannes Fantastic + FrontieresPalais K

Creator Economy SummitPlage des Palmes

Japan Country of Honour DayVarious venues, peak day Sun

Doc Day at Cannes DocsRiviera H4

Top pickOngoing trackSource: official MDF 2026 programme · curated picks per chapter 7

Named panels with speakers

If you only attend one panel, attend ours. Then attend these.

★ Molten Cloud panel

Sunday, May 1715:00The Viewpoint, Palais des Festivals

How AI Agents Give Top Sales Teams an Unfair Advantage

Avails decks built in hours, not weeks. Royalty queries answered before the buyer asks. Rights conflicts caught before contract signature. How the most data-fluent international sales teams are using AI agents to compress prep time and close gaps that used to need a full back office.

Arjun Mendhi

Founder & CEO, Molten Cloud

Sonia Mehandjiyska

Head of International Distribution, Electric Entertainment

Friday, May 1511:30 to 12:30The Viewpoint, LerinsAFCI · Global Film Commission Network Summit

The Power of Place: From Incentive to Execution

How producers work with film commissions to move projects from concept to screen. Incentives, infrastructure, and local partnerships shape decision-making.

Saturday, May 1615:30 to 16:30Main Stage, RivieraAFCI · Global Film Commission Network Summit

The Power of Place: Made in Japan

Japanese filmmakers, producers, and policymakers on how creative vision and production infrastructure intersect. Dovetails with Japan as Country of Honour.

Cannes Next platform launches. Throughout May 12 to 20, Village Innovation (Pantiero), Main Stage (Riviera), Plage des Palmes, The Viewpoint (Lerins). MDF badge.

The innovation programming for the entire market drops here, including AI, virtual production, and immersive demos that run all week. Cannes Next has the largest VP stage at any film market globally. If you're tech-curious or tracking how production-side innovation feeds back into rights, walk through the Village Innovation on Day 1 and bookmark which sessions to return to. For: tech-forward distributors, producers, anyone evaluating AI tools for rights or operations.

The European Film Commissions Network spotlight breakfast. Networking-dense. Worth the early start if you work European co-productions or any pipeline involving EU film commission funding. For: anyone with European co-pro exposure.

Thursday, May 14

WIFT Africa Breakfast. 09:00 to 10:30. Producers Club, Lerins Upper Floor. Producers Network badge.

Women in Film & Television Africa networking breakfast. Tight, focused, useful for distributors building African pipelines or for producers looking to engage African co-financing. For: distributors, producers, sales agents working African territories.

Cannes Docs opens. Riviera H4. Runs through May 19. MDF badge.

The dedicated documentary venue and program. Docs-in-Progress, Spotlighted Projects, Co-Pro Social Club, Meet the Pros speed meetings, daily Happy Hours. If you do any documentary acquisitions, position yourself here for at least one full afternoon. For: doc rights, doc acquisitions, festival programmers.

Friday, May 15 (First Big Day)

International Film Finance Forum. 14:00 to 18:00. Main Stage (Riviera). MDF badge. Hosted with Winston Baker.

The single highest-leverage four hours of the market for anyone whose work touches rights and finance. Sessions cover sales and distribution trends, finance strategies, creative capital, co-productions, and short-form content. Winston Baker's curation is the reason this consistently draws the institutional money in the room. Top pick for the rights-and-finance reader. For: sales agents, financiers, fund managers, producers raising capital, CFOs.

AI for Talent Summit, Day 1 of 2. 10:00 to 13:00. Plage des Palmes (Goeland Beach). Invitation only (qualified C-level executives, investors, senior tech professionals, select media). Cannes Next program. Runs again Saturday morning May 16.

AI in production workflows, ethical and responsible AI use, real-world use case showcases. The first formal MDF programming where AI is treated as an operational reality rather than a topic. If chapter 6 of this guide resonated, this is your two mornings. Note the access tier: this is not an MDF-badge open session, so registration request goes through Cannes Next ahead of the market. Top pick for the AI-in-rights reader. For: producers, legal affairs, distributors evaluating AI tools, tech executives.

The Power of Place: From Incentive to Execution. 11:30 to 12:30. The Viewpoint (Lerins). MDF badge. AFCI presents.

The first of three AFCI Global Film Commission Network Summit sessions across Friday and Saturday. How producers work with film commissions to move projects from concept to screen, with a focus on incentives, infrastructure, and local partnerships shaping decision-making. Production-side perspective, but useful for understanding how location and incentive strategies feed into rights and finance. For: producers, location strategists, film commissioners.

The Power of Place: Stories Without Borders. 15:00 to 16:00. The Viewpoint (Lerins). MDF badge. AFCI presents.

Second AFCI session. International co-productions and location strategy when filmmakers cannot access the place a story is set in. For: same audience as the morning session, plus co-pro producers.

Japan IP Market opens. 15-17 May. Aboard the Art Explora catamaran. MDF badge with pre-registration. Co-organized with TIFFCOM.

A new Cannes 2026 launch and one of the headline Country-of-Honour activations. Three days of pitch sessions and one-on-one meetings with seven leading Japanese IP holders (Amuse Creative Studio, Kadokawa Corporation, Nihon Bungeisha, Nippon Animation, Shochiku, Shufu to Seikatsu Sha, Toei Company). The first dedicated trans-Pacific IP-to-screen market at MDF. If your slate has any room for Japanese animation or manga adaptation, this is the most concentrated buyer-meets-rightsholder window in the calendar. Top pick for distributors with APAC adaptation interest. For: international rights buyers, sales agents, co-producers.

Saturday, May 16 (Second Big Day)

Investors Circle, Day 1. Plage des Palmes. Keynotes are MDF badge; pitching is invitation-only. Creative Europe MEDIA partner.

A high-profile summit bringing together elite film and media financing experts and private investors. Keynote panel plus exclusive pitching session for investors plus networking cocktail. The conversations here on library valuation and rights-as-financial-assets are 6 to 12 months ahead of where the broader market is reading them. Top pick for the consolidation and financialization reader. For: fund managers, private equity, catalog owners, CFOs, anyone considering rights securitization.

The Power of Place: Made in Japan. 15:30 to 16:30. Main Stage (Riviera). MDF badge. AFCI presents.

Final AFCI session, dovetailing with Japan as Country of Honour. Japanese filmmakers, producers, and policymakers on how creative vision and production infrastructure intersect. For: anyone tracking Japanese pipeline.

Cannes Fantastic and Frontieres. May 16 to 17. Palais K. MDF badge. Partners: Fantasia (Montreal), Sitges (Spain).

The genre community hub. Frontieres runs two pitching sessions: Proof of Concept (Saturday May 16, 10:00 to 11:50) for projects in advanced financing, and Buyers Showcase (Sunday May 17, 16:15 to 18:05) for genre films in post-production with exclusive extracts for sales agents and distributors. Fantastic 7 (with Sitges) presents seven genre works-in-progress. Genre IP is a franchise engine for rights and royalty complexity (sequels, spin-offs, licensing, games, merchandise), and the deals struck here have unusually long downstream rights tails. For: genre IP rights holders, buyers in the horror/thriller/sci-fi space, franchise operators.

Spotlight Asia. May 14 to 17. Palais Stage and Producers Club. MDF badge. Partners: Ties That Bind, Focus Asia, Creative Europe MEDIA.

Asian IP market, pitching sessions for new IPs, fund representative access, co-production frameworks. With Japan as Country of Honour this year, the Asian programming is particularly dense. Spotlight Asia opens Thursday May 14 and runs through Sunday, with the IP pitching session on Palais Stage and the happy hour and presentation at the Producers Club. Worth attending even if you're not actively building APAC pipelines, because the deal patterns surfaced here travel quickly to other regions. For: international sales agents, co-producers, Asian-pipeline distributors.

Sunday, May 17 (Creator Economy Day)

Creator Economy Summit. 10:00 to 13:00. Plage des Palmes. MDF badge. ABEL Studios partner.

The inaugural half-day summit on the intersection of cinema and the creator economy. Adapting digital IP into cinema, scouting emerging talent from platforms, audience engagement strategies. This is the most-discussed new format at MDF 2026. The structural implication for rights workflows is significant: creator content brings non-traditional deal structures, multi-platform-from-day-one models, and shorter license windows. Cannot-miss pick. For: producers and acquisitions teams evaluating creator IP, digital agencies, anyone whose pipeline now includes platform-native talent.

Investors Circle, Day 2. Plage des Palmes.

Pitching session for investors plus networking cocktail. If you missed Day 1, the cocktail is the second-best entry point. For: same audience as Saturday.

Japan Country of Honour Day, peak emphasis. Various venues. MDF badge. METI, JETRO, UniJapan partnership.

Japan as Country of Honour runs across the full market, but May 17 is the peak day for Japanese animation and genre cinema programming, with co-hosted opening night content earlier in the week. The concentrated buyer attention on Japanese IP creates clear pricing signals. For: distributors with APAC interest, anyone tracking how Japanese animation IP enters Western pipelines.

The Association of Indonesian Film Producers (APROFI) spotlight breakfast. Tight, regional, useful for any distributor building Southeast Asia pipelines. For: SE Asia-focused distributors and producers.

Tuesday, May 19 (Beyond the Molten window, included for thoroughness)

Doc Day at Cannes Docs. Full day. Riviera H4. MDF badge.

Day-long documentary celebration: keynotes, masterclasses with filmmakers in Cannes selection, awards, mixer, and screening. The most concentrated single day for doc rights work in the entire 2026 calendar globally. For: doc acquisitions, doc distributors, doc producers.

A note on badges and the rest of the Producers Network week

Three of the picks above (EUFCN on May 13, WIFT Africa on May 14, APROFI on May 18) require a Producers Network badge, a separate registration from the standard MDF badge that confers access to the Producers Club and the breakfasts. If you hold the PN badge, the three breakfasts not detailed above are also worth attending: CCIDA + Hong Kong Film Development Council on Friday May 15, Hellenic Film & Audiovisual Center + Thessaloniki Film Festival on Saturday May 16, and Japan Country of Honour on Sunday May 17. All run 09:00 to 10:30 at the Producers Club, Lerins Upper Floor.

Producers Network registration usually closes 2 to 3 weeks before the market. For 2026 that window has effectively passed; plan your 2027 attendance now.

Chapter 8

How to Approach Buyers in 2026

Buyers at MDF 2026 are not coming to your meetings to hear your slate. They have read your slate already, on Cinando, on your one-sheet, in the trade press leading into the market. The meeting is for one purpose: to test whether you can transact at the speed and precision the 2026 deal floor requires. Every meeting is a rights-clarity test. The companies that pass close deals. The companies that don't, schedule follow-up calls.

This chapter is about passing the test.

The 30-second answer test

The most useful question to ask yourself before walking into any buyer meeting at MDF 2026: if the buyer asks "what's available in [their territory] for [their window] starting [a specific date], given current holdbacks," can someone in this meeting answer in 30 seconds without checking three different files?

If yes, you're ready. If no, the meeting will end with "send me the avails when you have them," and you should plan for it not to convert.

There is no shortcut around this. The buyer is not testing the depth of your relationships, the strength of your slate, or the persuasiveness of your pitch. They are testing your ability to transact. In 2024 they tested it differently; in 2026 they test it on rights data.

Data as leverage

The other thing buyers want in 2026 meetings is data. Specifically: theatrical box office numbers, streaming engagement metrics, FAST viewership benchmarks for comparable titles, completion rates from previous deals, audience demographic breakdowns by territory.

Bring numbers to the meeting. The companies that walk in with structured performance data on their existing portfolio negotiate from a different position than the ones bringing only narrative pitch material. A buyer who is on the fence about your title moves to "yes" when you can show them a comparable from your catalog that performed against benchmark, with the data to prove it.

This is also where the 2024 to 2026 inversion shows up most clearly. In 2024, the seller with the strongest narrative had the leverage. In 2026, the seller with the strongest data has the leverage. The pitch deck still matters, but the data appendix is what closes the deal.

Buyer intelligence

The best sales agents at MDF 2026 walk into every meeting knowing the buyer's recent acquisitions, their slate gaps, their territory appetite, and their budget cycle. They don't pitch blind. They build systematic profiles before the market, and they update those profiles across markets and across years.

Cinando's relaunch makes some of this systematic for the first time. Buyer acquisition history is more queryable than it used to be. But the deeper layer (who's actively in market for what, on what timeline, against what fund) is still relationship-and-research work. Distributors whose teams maintain buyer profiles in a CRM rather than in someone's memory are at a measurable advantage.

A useful pre-meeting checklist:

Last three acquisitions by this buyer, with territories and deal types if known.

Any public statements about slate priorities in the past 6 months.

Known territory gaps (where do they appear to need content).

Likely budget posture (acquiring aggressively, holding, or trimming).

Any conversations from previous markets that left a thread open.

Five minutes per buyer, multiplied across 60 meetings, is five hours of pre-market work. Worth every minute.

The follow-up reality

Industry data suggests that 60% of market deals close in the four to eight weeks after the market, not on the floor. Most sales agents have no system for tracking post-market pipeline. They have a stack of business cards, a notebook of meeting notes, and a calendar reminder to follow up "next week" that gets pushed to the week after.

This is where deals fall through that should have closed. The fix is not complicated. It is a CRM-style deal pipeline that captures every meeting, every follow-up commitment, every offer status, every revision, and every contract stage, and that surfaces what needs attention each Monday morning.

The agents who walk back into the office on May 21 with their pipeline already structured close 30 to 50% more deals over the following two months than the agents who walk back with a stack of business cards. This is not a software pitch. It is operational discipline. The software helps; the discipline is the prerequisite.

What to actually do at MDF 2026

A short list. Read it before each day's meetings.

Open every meeting with the avails position, not the slate. The buyer wants to know what they can buy. Tell them.

Bring data. Comparable performance numbers, completion rates, territory benchmarks. If you don't have them, get them before May 11.

Take meeting notes that match how you'll re-find them three weeks later. Not on paper. In a system.

Schedule the follow-up before the meeting ends, not after. "I'll send the avails snapshot for [territory and window] tomorrow morning" beats "I'll be in touch."

Walk out with three things on every conversation: what they want, when they want it, and what would unblock them. If you don't have those three things, you didn't have a real meeting.

Chapter 9

Structuring Your Market Week

An MDF week without a structure is just an expensive eight days in Cannes. The market is dense enough that the difference between a strong week and a wasted week is almost entirely operational, not strategic. This chapter is about cadence.

Day 1, Tuesday May 12: logistical only

Resist the urge to book Tuesday meetings. The market opens, but the building doesn't really open until Wednesday morning. Tuesday is for badge pickup, accreditation, walking the Palais (it is bigger than it looks on the floor plan), finding the Cinando terminals, locating the Producers Club at the Lerins Upper Floor (you will get lost the first time), and scouting your meeting venues. If you don't know where Plage des Palmes is by Tuesday evening, you'll be late to a Friday morning summit.

What to do specifically: walk the Riviera level at the Palais, walk Pantiero (Village Innovation), find the entrance to Lerins, locate the nearest decent coffee within five minutes' walk of each. Test your phone signal (it will be patchy in parts of the Palais), and decide whether you're working off Cinando on your laptop or your phone, because the answer affects how you book meetings on Wednesday.

End your Tuesday with a printed copy of your meeting list. The phone battery doesn't last the whole day; the printed copy does.

Days 2 through 5, Wednesday May 13 through Saturday May 16: dense meeting season

This is where the actual market happens. The cadence that works:

30-minute meeting blocks, 15-minute buffers between them.

Maximum 6 to 8 meetings per day if you want to be useful in any of them.

Anything above 10 meetings per day is performance, not progress. By meeting 9 you are not actually present in the conversation.

Block your meetings by venue, not just by time. Five meetings at the Palais followed by two at the Carlton Hotel works. Five meetings ping-ponging between the Palais and the Plage des Palmes does not. The Croisette walk between venues is 12 to 18 minutes once you factor in May tourist density and the inevitable industry bumping into industry on the sidewalk.

The Croisette in May: 12 to 18 minutes between venues, plus the people you'll bump into. Block meetings by location, not just by time.

Lunch is a meeting. Use it. The 90-minute slot between roughly 12:30 and 14:00 is too valuable to spend alone on a hotel terrace. Either book a working lunch with a high-priority buyer, or use it to walk the Marché floor and notice who is meeting with whom. Both are productive.

Days 6 and 7, Sunday May 17 through Monday May 18: conversion

The first half of the week is for first meetings. The second half is for second meetings, drinks, dinners, and the conversations where deals actually move. By Sunday evening, you should know which of your Wednesday meetings are converting and which are not. The ones converting get a drink Monday night. The ones not converting get a polite "let's stay in touch" email and a clean exit.

Don't keep pitching meetings on Day 7. The buyer is exhausted, you are exhausted, and you are competing against every other agent in your buyer's calendar from the past five days. The conversion conversations on Day 7 are with people who already said yes to you on Day 3 or 4. Use the day to close, not to open.

Day 8 onward, Tuesday May 19 onward: the post-market gap

If you stay through Tuesday May 19 and into the back half of the market, the calendar shape changes. Doc Day at Cannes Docs runs Tuesday May 19. Some buyers stay through Wednesday or Thursday. The conversations are slower, deeper, and often more productive than the Friday or Saturday meetings, because everyone has more time.

If you leave on Day 7 (which is what most working sales agents and distributors actually do, and what the Molten team is doing this year), the Day 8-onward gap is where post-market follow-up begins. Within 48 hours of leaving Cannes, you should have sent updated avails snapshots to every meeting that asked for one, scheduled second-conversation calls with every meeting that converted, and updated your CRM or pipeline tracker with status against each.

First-timer tips

Things you will not figure out from the official MDF documentation.

Cinando is the database, not the app. The Cinando platform is what every working professional at the Marché checks before, during, and after the market. Buyer profiles, attendee lookup, screening invitations, deal history. Set it up before you arrive, not on Day 1. The interface is functional rather than elegant; learn it once and stop fighting it.

Badge tiers matter. A Marché du Film badge gets you into the Palais and most general programming. A Producers Network badge is separate and gets you into the Producers Club at Lerins Upper Floor and the daily breakfasts. A Festival badge is a different system entirely (Festival, not Marché). If you assume one badge gets you everywhere, you'll be turned away from at least two events.

Smart-casual is the actual standard, despite what the photos suggest. The red carpet photos are the Festival, not the Marché. At the Marché floor, smart-casual works for most meetings. A jacket if you have a buyer dinner. The exception is that some specific evening events (Investors Circle Networking Cocktail, certain country pavilion receptions) lean dressier. Read the room.

Screening invites are not optional. If a sales agent invites you to a screening of a title they're representing and you don't go, you've taken yourself out of the conversation for the next three years on that company's slate. If you can't make the screening, send someone from your team. If you can't send anyone, write a real email afterward, not a one-line "couldn't make it." This is invisible to outsiders and important to insiders.

The Croisette closes at 18:00 the same way the markets close at 18:00, which is to say, not actually. The work continues at the bars, on hotel terraces, at the Plage du Goeland sunset hour. If you are leaving the Palais at 18:01 and going back to your hotel, you are missing 30% of the deal flow. Read chapter 10.

Chapter 10

Cannes Off the Croisette

The market closes at 18:00 on the Palais floor. It does not close at 18:00 in Cannes. A useful guide to the second half of the day, organized by what you actually need: a place to drink, a place to eat, a place to meet for breakfast, a place to take a quiet call, and a place to land late.

★ By invitation · Molten × Electric Entertainment

Friday, May 156:00 PM to 9:00 PM CETCannes · address sent on confirmation

A cocktail with Electric Entertainment

An evening with the Molten Cloud and Electric Entertainment teams during Marché du Film 2026. A small group of distributors, sales agents, and platform operators we have worked with or want to work with. Drinks, conversation, and a few of the people you want to be in a room with this year.

Brown Sugar. Carré d'Or, in the heart of Cannes. Opens at 18:00, becomes a piano bar at 23:00, closes around 02:30. Popular with industry during congress weeks, which means Marché week sees it at full strength. Good for groups, good for an after-meeting drink that turns into a longer conversation. Set the bar for your team's evening here on Day 1 and people will know where to find each other for the rest of the week.

Brown Sugar, Carré d'Or. The benchmark after-meeting bar; piano hours after 23:00 keep the conversation going past midnight.

Le Petit Majestic. Rue Tony Allard, off rue d'Antibes. The unofficial industry late-night institution. It is unpretentious, the beers are inexpensive (around three euros, a price that has held longer than most things in Cannes), and the room reliably fills with a mix of locals, sales agents, journalists, and the occasional spotted name. Morgan Freeman has been seen here. It comes alive nightly during the Festival; expect it to be the same during the Marché. If your evening dies, this is where you go to revive it.

Bar Majestic at Le Majestic Barrière. Croisette. The classic hotel bar, dressier than Brown Sugar, more visible than Le Petit. Useful for the dressier industry conversations and for buyers who prefer a hotel setting. Plan ahead if you're meeting a senior buyer here; a corner banquette is the difference between productive and shouted.

Le Fouquet's Cannes. Inside Hôtel Le Majestic Barrière. The brasserie cousin of the Bar Majestic. Works for early-evening drinks before a buyer dinner, less so for late-night.

Beach clubs and beach lunches

Plage du Majestic. The Le Majestic beach. Industry-standard for lunch meetings. Reservations are gone by the first Saturday of the market; book before May 12 if you can.

Plage du Carlton. The Carlton beach. Slightly more international-corporate, slightly less film-business. Same reservation reality.

Bâoli. Eastern end of the Croisette. Operates a mid-festival takeover that runs through the second half of the market. Not every day. Check the door. When it's on, it's where the louder dinners happen.

Plage des Palmes (Goeland Beach). Where the AI Summit, the Creator Economy Summit, and Investors Circle are programmed (see chapter 7). For non-programmed days, the beach is open for casual industry lunch. Useful if you want to meet someone outside the Palais traffic.

Inside the Palais (lunch and meeting spots)

Bistrot du Lérins. On the Festival grounds, Lerins level. Ocean-view, preferential lunch rates for badge holders, panoramic Mediterranean harbor view. The convenient lunch spot for back-to-back Palais meetings. Reserve in advance during peak market days.

The Viewpoint (Lerins). Programmed with workshops and happy hours throughout the market. Useful for a 30-minute meeting between sessions, or for a happy hour wind-down before the dinner circuit starts.

Producers Club (Lerins, Upper Floor). Producers Network badge required. Hosts the daily breakfasts (see chapter 7), happy hours, and the elevator-pitch sessions. The hardest room to get into and one of the most useful if you have access.

Morning and breakfast meeting spots

Marché Forville and the streets immediately around it. The local food market a few blocks from the Croisette. The cafés in the surrounding streets are where Cannois go for coffee when the Croisette is overrun. Cheaper, faster, and frequently better than the hotel breakfast rooms. A useful place to take an 08:00 meeting with someone who doesn't want to do another hotel coffee.

Hotel breakfast rooms. The Martinez, the Carlton, the Majestic, and the Grand Hyatt Cannes Hôtel Martinez all run formal breakfast service for guests and (with discretion) for industry meetings. Pricier, more visible, useful for a meeting where being seen is part of the point.

Quiet rooms (where to take a video call)

The Palais signal is patchy. The Cinando lounges have desks but are not quiet. Two practical options:

The lobby lounges of the Carlton, Martinez, and Majestic are functionally industry coworking spaces during the market. Most desk staff are tolerant of laptop work if you have ordered a coffee.

The Plage des Palmes terrace, in non-programmed hours, is one of the few places near the Palais where you can take a 20-minute video call with reliable signal and no overheard private conversations from the next table. If you have a buyer call scheduled at 11:00 between two physical meetings, this is the move.

Restaurants for buyer dinners

Reservations close fast. The first Saturday of the market is usually the cutoff for the higher-tier restaurants for the rest of the week. If you have not booked by May 11 for May 13 to 17, your options compress significantly.

The standard tiers, broadly:

Tier 1 (high-end, formal). The hotel restaurants (Le Park 45 at Le Majestic; the Carlton's signature dining; the Hyatt Hotel Martinez restaurants) are the safest for senior-buyer dinners that need to feel important. Da Laura is a reliable Italian standby. Tetou (in nearby Golfe-Juan, requiring a 15-minute taxi) is the classic lobster pilgrimage; book before April or skip it for 2026.

Tier 2 (industry-standard, useful). L'Affable is a bistrot routinely cited as a working-meeting favorite. Astoux Brun runs late and does seafood, useful for the post-meeting late dinner. Fouquet's at Le Majestic if you want to keep things on the Croisette.

Tier 3 (casual but functional). The cafés around Marché Forville. Pizzerias on rue Meynadier. The unbookable spots that you walk into at 22:00 because dinner ran late.

Late night

After the dinner circuit clears around midnight, the late-night map narrows to a few options. Le Petit Majestic, Brown Sugar's piano bar hours, and the post-dinner crowd at the hotel bars. Some clubs flip into industry party hosts on specific nights (these are typically invitation-driven and circulated by word of mouth on the day of). If you don't have an invitation and you want to keep working, the late shift at Le Petit Majestic is the one that pays back.

A small note on the 18:00 to 20:00 window

If you have not been invited to a yacht party, that is fine. The conversations on the Croisette and at the Plage du Goeland terrace between roughly 18:30 and 20:00, before dinner reservations start, are often more productive than the parties they precede. Some of the most useful 30 minutes of the entire week happen here, with a drink, no formal agenda, and the day's meetings still fresh enough to discuss honestly. Use the slot.

Chapter 11

Where This Is Heading

Ten chapters of tactics. Now the analysis. If you walk the Croisette this year and pay attention to which programs are oversubscribed, which conversations are happening, and which deals are closing on the spot rather than in follow-up, the next 24 months of the international market are visible. Most of them are extensions of trends already in motion. A few are inflection points. This chapter is the read.

The creator economy stops being a side track

The single most-discussed structural change at MDF 2026 is the inaugural Creator Economy Summit on Sunday May 17. Three hours of programming, half a day of attention, one new Cannes initiative. By itself, that is a programming change. In the context of what is already in motion, it is a market signal.

The creator side of the audience has been growing at SVOD-eclipsing rates for five years. Top-tier creators on YouTube, TikTok, and Instagram now pull weekly audiences that match major streaming series, with engagement metrics that a traditional theatrical release cannot manufacture. Through 2024, those audiences stayed inside the platforms that grew them. Through 2025 and 2026, they started crossing over. ABEL Studios, the partner on the MDF Creator Economy Summit, exists specifically to support creators developing, financing, producing, and distributing long-form content. They are not the only such operator; they are the formalization of the trend.

What changes operationally for distributors in 2027 and beyond:

Acquisition supply expands. Creator-originated IP enters the buyer pipeline. Adapted from a successful YouTube channel, a podcast, a TikTok serial, the underlying content has audience metrics attached at acquisition time, which inverts the traditional distributor pitch.

Deal structures shorten. Creator content tends to come with multi-platform-from-day-one expectations and shorter license windows. The old "we'll take all rights for ten years" output deal does not survive contact with creator-economy IP.

Audience data becomes a sale asset. A creator title comes with engagement signals you can pitch to FAST and AVOD platforms directly. The distributors who learn to read and resell creator analytics are the ones doing creator-IP deals in 2027.

The Creator Economy Summit is a half-day in 2026. By 2028 it is an entire track.

AI moves from clause to substrate

Chapter 6 covered AI as a contract conversation. The trajectory beyond MDF 2026 is AI as substrate: not just clauses in deal memos, but production tooling, marketing tooling, distribution tooling, and verification tooling embedded into the deal infrastructure itself.

Three concrete moves to expect inside 18 months:

Synthetic-performer economics break a threshold. The Tilly tax debate is about defending the cost equivalence of a real actor versus an AI one. Whichever way the proposal lands at SAG-AFTRA, AI-generated performance becomes economically rational at certain budget tiers, and the rights infrastructure needs to track who consented to what, where, when, and for what use.

Back-catalog AI training rights become a revenue line. Library owners with structured rights data and clean chain-of-title can license training data legally and confidently. Library owners without that data get the same offers and stall on legal review. The deals being struck in 2026 set the precedent rates for the next decade.

AI-augmented distribution tooling becomes table stakes. Avails decks generated in minutes. Buyer profiles enriched automatically. Royalty reconciliation across 15 platforms with anomaly detection. The distributors using these tools at MDF 2027 are not visibly different from the ones not using them, except in the conversion rate of their meetings.

Performance-based licensing becomes the default

Through 2026, performance-based deal structures are still partially treated as exceptions. SVOD output deals carry fixed fees with bonus tiers; FAST deals are revenue-share. By 2027 to 2028, the pattern flips. Output deals carry fixed minima with performance overlay; FAST deals stay revenue-share but expand into completion-rate, audience-quality, and territory-tiered rate cards. Every license, on every platform, in every territory, has a data pipeline behind it.

The infrastructure implication is the one most legacy systems are not being upgraded for. Royalty calculation across a portfolio of performance-based deals is not an accounting task. It is a streaming-data engineering task. The companies that internalize this in 2026 are not playing catch-up in 2028.

The library becomes a financial asset class, openly

Allegro Finance with Elliott Advisors at $500 million in March 2026. MediaHedge with a $200 million JV credit fund in April 2026. Hipgnosis-style funds buying backend participation rights. Through 2026 the institutional capital arriving at the rights side of the industry is still individually noteworthy. Through 2027 it is structural. The buyer at the Investors Circle keynote panel in 2027 is the buyer who quietly drives mid-size acquisition pricing for the rest of the year.

What this means for distributors with libraries: rights data becomes due-diligence collateral. The catalog that closes a financing deal in 2027 is the catalog that can present chain-of-title, clean rights records, complete contract metadata, and platform-by-platform revenue history in a single export. The catalog that cannot, gets a discount on valuation regardless of underlying content quality.

The mid-size split widens

The pattern through 2026 is already visible. Two mid-size distributors with similar catalogs and similar revenue can have wildly different outcomes at the market based entirely on operational precision. The gap widens in 2027.

The companies pulling ahead share three traits: structured rights data accessible in real time, performance reporting infrastructure across every active platform, and post-market follow-up discipline. The companies losing share have none of these and are competing on relationship and slate. Relationships and slate still matter. They are not, on their own, sufficient anymore.

Three signals to watch in the next 12 months

Three concrete things to track between this Cannes and the next.

First, what comes out of the Creator Economy Summit. The follow-on programming announced over the next 12 months tells you whether MDF treats the creator side as a category or as the new main act.

Second, the Tilly tax outcome and any equivalent IATSE / DGA AI provisions. Whatever lands in the SAG-AFTRA contract will set a precedent that ripples through every territory's union and guild structures.

Third, the buyer composition at Investors Circle 2027. Who shows up in that room signals where institutional capital believes the rights side is heading. The names in the room change quietly from year to year, and the changes are the leading indicator.

The structures of MDF 2026 will look obvious in retrospect by MDF 2028. The companies reading those structures correctly now are the ones still in the room.

Table of Contents

The Molten Survival Guide

Cannes / Marché du Film 2026 · 10 chapters · ~35 min read